This is a sponsored post by Cents. Find out what Cents can do for your laundry business here. All reviews and opinions expressed in this post are based on my personal view.

Laundromats might be the best small businesses in America. They are relatively simple, produce a high cash flow, require little overhead, and more. If you buy your first laundromat the right way the first time, the sky is the limit. Your high cash flow and flex time can allow you to expand into more laundromats, add new services, or even invest in other businesses. However, if you buy wrong the first time, you may find yourself struggling to dig yourself out of a hole. It can be a real uphill battle.

The key to buying your first laundromat right the first time is doing proper due diligence. It is critical to have the right information about the business and make a proper valuation based on that information. Being off just $500 per month could mean overpaying by $20,000-$30,000. It’s not hard to do.

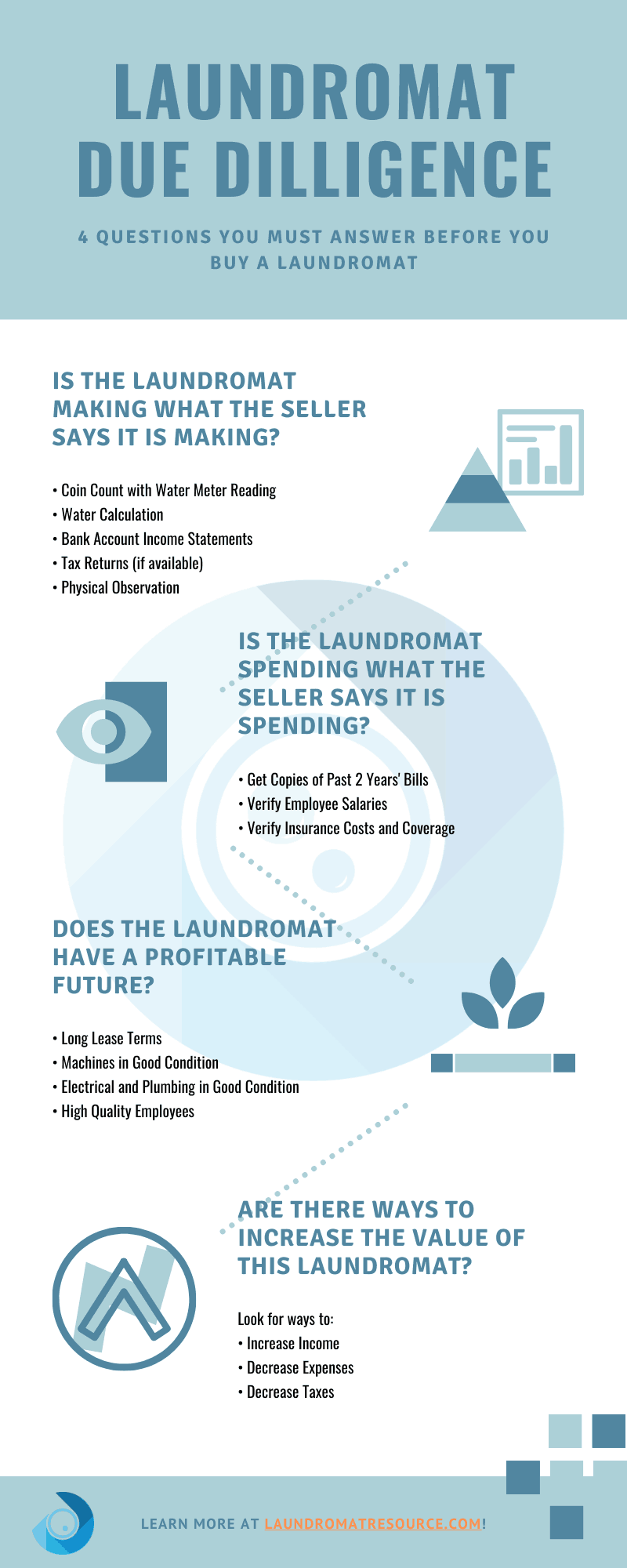

So how do you do proper due diligence to ensure you are buying the right laundromat for you at the right price? You need to go through the 4 Pillars of Laundromat Due Diligence. The 4 pillars are:

- Determine the laundromat’s income

- Determine the laundromat’s expenses

- Determine the laundromat’s trajectory

- Determine value-add opportunities

We’ll go through each of the 4 Pillars of Laundromat Due Diligence in this post. By the end you will be crystal clear on the basics of what due diligence you need to do when buying your first laundromat.

Laundromat Valuation

When doing due diligence on a laundromat, what you’re doing is assigning a number to the performance of the laundromat. You must base the value of the laundromat on its performance and not its potential.

Performance is measured by the laundromat’s Net Operating Income (NOI). The net operating income is the gross income of the laundromat minus the gross expenses, not including taxes and loan payments. By determining the NOI, we can assign a value to the laundromat.

Due diligence is the process of verifying the NOI and, if necessary, adjusting our valuation based on what we uncover.

The one caveat to this form of valuation is that a laundromat that makes very little money, breaks even, or possibly even loses some money does still have some value. That value will be based more on the assets than its performance. The assets include the washers, dryers, boiler, change machines, vending machines, etc. But, those assets also include the infrastructure of the space (ie- plumbing, electrical, gas, floor drains, etc.) and goodwill in the community.

Pillar 1- Determine the Laundromat's Income

The first Pillar of Laundromat Due Diligence is determining the laundromat’s income. We need to know how much money is coming into the laundromat. This seems obvious, but it can be easier said than done. Since the majority of laundromats are still cash businesses, utilizing coins either entirely, or as one option of payment, pinpointing the exact amount of income can be a challenge.

If you look at even a handful of deals, you will definitely find laundromats that have limited financial records, scattered financial records, incomplete financial records, conflicting financial records, and even no financial records whatsoever. This is the reality of this business, and it’s what makes your due diligence so critical.

So how do we determine a laundromat’s income then? There are three primary ways to determine the income of a laundromat. I recommend using all three together whenever possible to get the most data possible. None of them are entirely accurate, but together than can narrow in the range of probable income of a laundromat.

These are the three main methods of determining a laundromat’s income:

- The utility usage method

- The coin count method

- The document method

Let’s go through each of these 3 methods of income verification so you have a firm grip on what each of them has to offer, and also their limitations.

The Utility Usage Method

The first way to verify a laundromat’s income is to use a water analysis. This technique is not precise but will give you a decent ballpark of how much money a laundromat is making. Let’s talk about the basic concept behind the water analysis and then I will direct you to a free tool to make it easy for you.

When you enter due diligence with a laundromat, you will need to request the utility bills from the seller, preferably for the past 2 years at least. All of the utility bills will give you useful information about how much the laundromat is being used, and therefore how much money it is making each month.

Of particular interest is the water bill. The water bill is going to tell you how much water has been used each month. This will be important information to have to run your analysis.

Ok, here’s the concept. Laundromats consist of various size washing machines. For each size of washing machine, you’ll need to determine how many gallons of water are used per wash cycle. The best way to do that is to check the manual if it’s available. If it’s not, the next best thing is to find the model number and serial number of each size of machine.

With the model number and serial number, you’ll need to look up the water usage. The best first attempt of that is to search the brand name of machine + model number + water usage. If you can’t find the information online, then your next best bet is to call the machine manufacturer with the model and serial number and ask them for the water usage numbers.

You need to do this for each size of machine in the laundromat. It’s a little bit labor intensive but can help you determine the income of the laundromat.

Once you have found out the water usage, the next piece of information you need is the average number of times per day each machine is used. With those two pieces of information and the vend price, you can find out the approximate income of the laundromat. The formula looks like this:

# gallons used by machine size #1 X average turns per day x vend price = monthly income of machine size #1

Do this for each size of machine and add them together to get the total wash income. Multiply the total wash income by .35 (35%) to determine an approximate dryer income. This should be close to the reported income.

One final note on this analysis is that you can compare the sums of the gallons used by each machine size multiplied by the average turns per day to compare the water usage number with the actual numbers reported on the bills to make sure everything lines up. Compare:

# gallons used by all machines (assuming X turns-per-day) ≈ # gallons used on the actual water bill

If there are major discrepancies, you’ll need to explore further.

Now, I promised a free tool to make it easier for you! We have a free spreadsheet that you can download when you’re logged into your free membership account. It’s located in the Member Resources tab in the main menu when you’re logged in along with a host of other great resources! Take advantage of those!

The Coin Count Method

The second way to verify income is through a series of coin collections with the seller. I’ll explain the concept behind this and then I’ll tell you where you can download a free tool to keep track of everything (in case you can’t guess where to find it).

A coin count starts with the buyer and seller meeting at the laundromat and collecting all of the coins in the store. This allows you to start with a clean slate. You’ll also need to take a reading off of the water meter and write that number down. This will help you keep track of how much water is going through the store between collections.

After an agreed-upon number of days, the buyer and seller return to collect the coins and take a water meter reading together again. I always recommend collecting coins by the size of machine. For example, collect and count all of the 20 lb. machines together. Collect the 40 lb. machines together. Etc. And don’t forget to take another water meter reading.

You’ll proceed with this pattern anywhere from 2-6 weeks usually, with 3-4 weeks being the most common length of coin collections. With that data, you should be able to extrapolate out the income for the month and verify the seller’s reported income. You’ll also want to extrapolate out the water usage from the meter and make sure it’s in the ballpark for the past months according to utility bills.

As always, if there are discrepancies you’ll want to get to the root of them. You may need to correct your math, renegotiate, or back out of the deal altogether.

The risks here are that the seller is adding quarters behind the scenes and running water in the backroom to make it look like the laundromat is performing better than it is. The best way to deter that or catch it is to require access to the security camera system during due diligence. If there isn’t one, consider installing a temporary security camera system during due diligence.

And again, we have a free Coin Collection Worksheet for you to download when you log in to your free member account. It has space for you to record collections by size of machines and also a space to record water meter readings. It’s a handy way of keeping yourself organized.

The Document Method

The third way to verify a laundromat’s income is through obtaining a paper trail from the seller. If they use a card system this will make it easy. However, most laundromats still don’t have any kind of card system.

Other documents you can request to help you verify income are the business taxes and bank deposit statements. The sellers may or may not give you access to this information but you can always ask. If they refuse to disclose those documents, it’s not necessarily a deal-breaker, but it is a signal to proceed with caution and be extra diligent.

The bank deposit statements will help you determine how much money is being made. It won’t be 100% accurate, but, again, it will help narrow the range. The taxes generally are more helpful in determining what expenses to expect in the business than determining how much the business is making.

Download and share this infographic!

"If the seller is willing to lie to the government, they're willing to lie to you."

Another common scenario is that a seller agrees to disclose taxes and/or bank deposit statements but lets you know with a nod and a wink that those numbers might be low. This is implying they are skimming money off the top. Again, this isn’t a deal-breaker, but, as I always tell my coaching clients, if a seller is willing to lie to the government about how much money their laundromat is making, they’re willing to lie to you, too.

Pillar 2- Determine the Laundromat's Expenses

Knowing a laundromat’s income is only half the equation to determine the performance of the laundromat, or the net operating income. We also need to determine the expenses of the laundromat. This may seem more straightforward than trying to determine the income, but it can be easy to miss significant expenses or to underestimate those expenses. And, remember, if you’re off by just $500/month, that’s a value drop of $20,000-$30,000! It’s essential that you realistically determine the expenses and verify them before you commit to buying a laundromat.

I have personal experience in failing to verify expenses properly and losing value. And, I have had many, many consulting clients who have booked time with me and we have caught previously missed expenses. I have also, unfortunately, had more than a few consulting clients who have booked calls with me after they found out that they had miscalculated expenses. At that point, we pick up shovels and start digging them out of the hole they found themselves in.

There are 4 main things you should be doing when you verify expenses.

- Request bills and statements

- Request to see the lease and all amendments and addendums

- Verify expenses using a pro forma

- Utilize an experienced expert, such as another laundromat owner or consultant

Request Bills and Statements

Some expenses are relatively easy to verify. You just need to make sure you don’t miss them in your analysis (which we’ll get to in number 3!). For utilities and other regularly occurring bills, you can request to get a copy of the actual bill or statement. You should request the actual bills, which the seller should be able to download as PDFs and provide to you to look over. The same is true of other bills that the laundromat might have, such as phone and internet, insurance, or security bills.

I recommend you request at least 2 years’ worth of bills.

When the laundromat owner provides you with the bills, you’ll want to look through them thoroughly. You need to be looking for consistency, or, more importantly, inconsistencies in the bills. For example, you should take note if the most recent 3 months’ utility bills are 10% lower than the months before it, or than the same 3 months the previous year.

You can also look for patterns to help you determine how the laundromat performs over time. For example, you might observe that the income from October through April is about 15% higher than in May through September. In some places, this would be pretty normal. By knowing this pattern you could plan accordingly.

The utility bills, in particular, can also help you assess the performance of the business. You can use these bills to help you verify the laundromat’s income. The variability of the utility bills will be tied to the variability of the laundromat’s income

Request the Lease & ALL Amendments and Addendums

The lease is the most important document in your business. Your rent plus any common area maintenance (CAM) or triple net costs will be one of your largest expenses. It is also a binding contract that you will be expected to adhere to. Verifying the expenses of a lease is relatively straightforward as long as you actually read through the lease and understand the terms of the lease. Your financial responsibilities will all be outlined in the lease and documents referred to in the lease (amendments and addendums).

I always recommend that you read through the entire lease yourself. Yes, I know. Yawn. Inject some caffeine in your veins if you have to but that lease is basically a marriage contract. Know what you’re walking into before you say “I do”.

I also recommend that you get two more specific people to read through your lease for you.

- A contract lawyer- A good contract lawyer will be on the lookout for legal gotchas and loopholes that you could fall through. Keep in mind, it’s their job to nitpick contracts so you don’t always have to push for every change they make to a lease, but pick the important things and stand your ground. The best way I’ve found to find a good lawyer is through a referral (try asking on the forums or in one of the Facebook groups for laundromat owners) or through a collective recommendation through a review website like Yelp or Google reviews.

- A knowledgeable laundromat professional- While a lawyer can spot the legal mines in a lease agreement, someone who has a firm grasp on the laundromat industry can spot the laundromat business-specific gotchas that a lawyer may not know to look for. I have saved consulting clients hundreds of thousands of dollars in actual or potential losses just by knowing what pitfalls can lurk in a lease agreement. I do offer consulting services, which include reading through a lease, but there are many great options that can help you here. Another consultant, broker, or owner willing to help you can literally save you tens of thousands of dollars potentially.

Don’t cut corners on understanding the lease. It’s critical and worth investing a little in to thoroughly understand it.

Verify Expenses Using a Pro Forma

Here’s a quick story for you. Some clients of mine were buying a laundromat. We had negotiated a price with the sellers and all parties signed the purchase agreement. The laundromat went into escrow and began doing our due diligence. A week before close we (and, unfortunately, the sellers) found out about a sewer bill that was being sent to the landlord that never made it to the sellers. Unfortunately for the sellers, they had to pay a large, unexpected water bill just before the close of escrow.

That bill came out to average about $700 per month of unaccounted for expenses. This dramatic increase in expenses caused the net income to be significantly less than anticipated. We had to negotiate a much lower offer price just before the close of escrow. Our new price was close to $50,000 below our original offer price!

That was painful for the sellers and my clients and I both felt bad for the sellers (who are great people!). However, had that expense been missed, my clients would have not only been making $700 less per month than expected, they would have also immediately lost $50,000 in equity in their business!

I tell that story to illustrate the importance of accounting for all expenses. missing one could have disastrous consequences. One great way to make sure all expenses are accounted for is to use a pro forma to ensure you don’t miss any big expenses. A pro forma will have line items for common laundromat expenses. You can use that to verify that a laundromat’s expenses are accounted for.

Not every laundromat will have every expense on a pro forma, but it’s worth verifying whether the laundromat you’re interested in does or not.

You can download a free sample pro forma to use in your expense analysis when you join as a free or pro member here at Laundromat Resource! Log in and click “Member Resources” at the top menu to get access to the sample pro forma and a bunch of other free tools and resources to help you find financial freedom through laundromat ownership!

Utilize an Experienced Expert

The more knowledgeable eyes on your deal the better. Tapping into your network of other laundromat owners to get some input on your deal is a great way to analyze the expenses of a laundromat. You can start a thread on the Laundromat Resource Forums. You’ll get some great input on your deal, questions to explore, and advice on how to proceed forward. This can be a great tool for you to get input on your deals!

Another great tool can be a consultant or coach who has laundromat business experience. This needs to be someone who is not compensated based on you buying a laundromat or equipment. Your broker or distributor can be great resources for you during the transaction, but it is valuable to have an unbiased opinion of a deal.

We obviously offer consulting services that we believe are incredibly valuable. However, there are other great consultants out there that could be a great help to you in your laundromat acquisition. We’re not the only game in town.

One other potential source of consulting could be a broker who is compensated outside of the deal who acts as a consultant and not the broker.

Pillar 3- Determine the Laundromat's Trajectory

Once we have determined the laundromat’s income and expenses and we have determined the NOI, you may think that we’re ready to determine the value of the laundromat. But we’re not quite ready to do that yet. Before we can assess the health of the laundromat, we need to look at the trajectory of the laundromat. What do I mean by trajectory? Great question!

The trajectory adds a third dimension to our analysis that is critical to a proper valuation: time. We need to take a look at the performance of the laundromat over time. To do that, we need to look at 4 key metrics to see which direction(s) they are trending.

- Income trajectory

- Expense trajectory

- NOI trajectory

- Utility usage trajectory

Income Trajectory

When you do due diligence on a laundromat, you definitely want to verify how much income a laundromat is making. But verifying the income only gives you the big picture. We need to introduce the element of time into our laundromat analysis.

Let’s consider a quick example. Let’s say you get financials from a seller that says that the laundromat made $100,000 of gross income in the last year. Maybe the net is $20,000. It’s a solid, though not perfect laundromat, and we determine the proper multiple is 4.5. Accordingly, we offer $90,000 ($20,000 x 4.5 multiple). Sounds like a pretty solid deal.

However, what if we introduce time into the equation and plot the monthly income? Notice the following income:

You can see that the average income for the year is $100,000, but it’s not very reflective of how the business is actually performing when you take over.

In this scenario, I would probably take the last 6-7 months and extrapolate the income for a year from those numbers.

However, that’s only half of the battle. Our next task is to determine what happened around June to make the income decrease so dramatically. There are a variety of reasons that could cause this, such as a new competitor, the owner getting sick, an owner’s death, loss of a key employee, and more. The point is, we need to search out the “Why?” Once we’ve determined the root cause, we can make a determination as to whether or not we think we can overcome those reasons. If we think we can, it’s time to put a plan into place as to how we’re going to do it.

Expense Trajectory

Income is only one variable, however. The health of a business is not determined by how much money it brings in, despite what the gurus tell you. Gross income can be a great number to brag about, but the only number that really matters is the net income. In order to determine the net income, we need to also determine the expenses over time.

Let’s take our previous example of a laundromat that brought in an income of $100,000 over the last year but saw a steep drop-off of income in June. To get a fuller picture, we need to see what the expenses are doing during those times, too. For example:

The plot thickens again! It turns out that even though the income when down dramatically in June, so did expenses. In fact, the laundromat has a net income that’s greater in the last six months than in the first six months.

That’s great news for the laundromat! However, we need to follow through with our due diligence and find out “Why?” the expenses dropped so much compared to the income. Perhaps they decided to go from fully attended to partially attended or from partially attended to unattended. We don’t know (mostly because I made this up), but the point remains, we need to find out the “Why?”

NOI Trajectory

As I mentioned above, the NOI in this particular example actually increased despite the dramatic drop in gross income. This could be plausible, but if I found myself in this scenario I would be skeptical. It would be time to strap on my sleuth had and dig a little deeper.

However, this does illustrate how determining the gross income, averaged over a year can tell one story, while plotting the trajectory over the same year can tell a different story. It also shows how averaging the expenses over a year can tell one story and plotting the trajectory of the expenses over the year can tell a fuller story. In this example as seen in the graph above, the story the NOI tells (assuming the numbers are verified) is that the NOI essentially doubles despite the drop in income. and remember, the NOI is what matters.

Again, in this scenario, even assuming all of the numbers have been verified, I would want to explore the sustainability of these new numbers. Can the income stay the same while keeping the relatively low expenses indefinitely? That is the “Why?” we need to answer when determining the NOI trajectory.

Utility Usage Trajectory

A final step in the third pillar of laundromat due diligence is to plot the utility usage over time. Typically, utility bills should be in the 15-20% of the gross income range. It’s good practice to plot the utility expenses to ensure there is nothing amiss. It’s fairly easy to do. When you request the utility bills, just add those numbers into a spreadsheet and make sure they follow the general trajectory of the income. If they don’t, it’s time to pull out our old trusty tool, “Why?”

When plotting the utility usage trajectory, you’re looking for two main things.

- Inconsistent trajectory with income trajectory- If the utility usage zigs when income zags, there may be something amiss. It could be a misrepresentation of income, but it also could be a water leak, the addition of new equipment, mass adoption of detergents that don’t need hot water, warm weather requiring less dry time, etc. The point is, I know that you’re getting tired of hearing it but you just need to answer the question, “Why?”

- Sudden spikes in utility usage- Sudden spikes could indicate an issue that needs to be addressed, like a leak. There could be serious consequences if left unattended to.

Pillar 4- Determine Value-Add Opportunities

We discussed way back up at the top of this post how laundromats are valued. As a quick recap, laundromats are valued based on the net operating income, or gross income minus expenses. This means that looking for ways to increase income in your laundromat has a two-fold benefit to you.

- Your net income goes up. This results in more money in your pocket every month.

- You build equity in your business. This results in your net worth increasing.

Looking for ways to add value to a laundromat during due diligence will give you an edge, both in your negotiations and also when you take over the laundromat and begin implementing your value-add opportunities.

There are four main categories of ways to add value to your laundromat. We’ll go through them here, but there are many specific ways to add value (ie- increase income and/or decrease expenses) to a laundromat. We have a free Value-Add Checklist that you can download when you are logged in to your free account. Like all of the other resources mentioned in this guide, it is located in the “Member Resources” and “Pro Resources” links in the menu when you’re logged in.

The four main categories of value-add opportunities are:

- Improve Management

- Add Revenue Streams

- Offer New Services

- Trim Expenses

Improve Laundromat Management

Often times the lowest hanging fruit when it comes to adding a lot of value to a laundromat is improving the management of the laundromat. There are a few basic things you need to do to keep your laundromat running smoothly and to keep your customers happy. Some of the basics are:

- Keep your laundromat clean

- Keep your laundromat safe and well-lit

- Have friendly, welcoming, and helpful attendants

- Keep your machines in good working order

- Ensure you have change available or your card/app payment systems are functioning properly at all times

- Continually look for ways to improve your business in both big and small ways

There’s more to running a successful laundromat business than that, but if you take care of those basic things consistently you’re going to be ahead of the curve.

Managing a laundromat so that customers have a better experience can be a great way to build goodwill with your current customers and to attract and keep new customers. This will inevitably improve your NOI, and, as we know, therefore increase the value of your business. If you need help managing your laundromat business take a look at Cents. Cents is a business-in-a-box laundromat management solution that allows you to elevate the level of service you can offer to your customers while cutting down the time it takes to do it.

Add Revenue Streams

Once you have improved your management of the laundromat or improved the management of the previous owners, you can start looking for ways to add more revenue streams to your main self-serve laundry business. Adding more revenue streams will contribute to increasing your NOI and can increase the value of your laundromat pretty quickly with some small additions.

Let me give you a small example to demonstrate how powerful this can be.

Let’s say you add a gumball machine to your laundromat. Kids love it, obviously. I have a little pinball gumball machine in one of my stores and my own kids love it. Let’s say that your gumball machine is nothing crazy, but it brings in about $85 of net income per month. That’s just under $3/day. Seems pretty doable.

Over the course of a year, that comes out to about $1,000 of net income that goes straight to your pocket. You can have yourself a nice little weekend getaway, buy yourself a pretty decent gift, or invest in a course. Whatever you want to do with that $1,000, the world is your oyster. You’re $1,000 richer that year.

But, since your NOI went up by $1,000, the equity in your business increased by 3.5-5 times that $1,000. So now your business is worth somewhere between $3,500-$5,000 more! That’s a double whammy!

I give this example to show how even adding a small amount of income can make noticeable improvements in the value of your laundromat. And there are many revenue streams you can add to your laundromat, both big and small, to increase not only your net income but also the equity in your laundromat.

The added benefit of some of these new revenue streams is that the right ones can make your laundromat more attractive to customers and improve their overall experience at your business. This means you’re improving the experience while making more money! That’s a huge win/win!

Offer New Services

Offering new services can be the biggest opportunity to add income to your laundromat business, and therefore to add value to your business. Services like a drop-off laundry or laundry pick-up and delivery allow you to serve a new demographic of people and allow you to draw from a larger customer pool by extending your laundromat’s radius of influence. Starting a laundry drop-off, or wash-dry-fold, service or a laundry pick-up and delivery service can be a bit undertaking, but the payoff can be huge.

The possibility for growth can be essentially unlimited, but these services do increase the complexity and management needs of the business. Each owner needs to weigh for themselves if they want to offer these services, but the potential for growth is undeniable. These services have been growing rapidly over the last couple of years and, I suspect, will continue to do so. If you’re interested in how to add these services to your laundromat the easy way, check out this webinar I hosted with two rockstars from Cents.

Make no mistake, however, these services are not passive income. They require work, management, and a relentless pursuit of improvement.

There are other services you can offer, too, that may not require as much management. For example, an alteration service is a common laundromat service offering if you have someone who is able to alter clothing. Another example would be adding a small convenience store or coffee shop inside your laundromat. The opportunities are only limited by your creativity.

Trim Expenses

The first three ways to add value were ways of increasing income. But you can add value by decreasing expenses, too! There are lots of ways to spend less money in your business so let’s talk about a few of them to get your creative juices flowing.

- Change business models- Consider going from fully attended to partially attended, or from partially attended to unattended. This move doesn’t make sense in many scenarios but it may make sense in yours. Run the numbers to find out.

- Renegotiate the lease- Renegotiating a laundromat’s lease can provide you with a lot of bang for your buck. Typically, laundromat leases are long-term leases, so any savings you can secure in the lease can really pay off over time.

- Refinance high rate loans- Refinancing can be a great way to lengthen out loans while decreasing monthly payments. While this one doesn’t necessarily build equity in your business directly since loan payments aren’t calculated in the NOI, extra money in your pocket every month never hurts.

- Buy new machines– I made a video on this one that is definitely worth watching, but long story short, buying new machines can actually save you money every month when you buy them strategically. Do the math and the math will help you make the right decision here. That video I linked will help you figure out what the right math is.

- Shop around- Many of your bills can be shopped around. While you may be stuck with your utility companies, you can shop around many of your bills. You can talk to multiple distributors when buying new machines. You can shop your insurance bill, internet bill, cable bill (get rid of the cable in your laundromat and do yourself and your customers a favor and get AtmosphereTV for free when you use my affiliate link), and more. My one caution is don’t sacrifice what you need to save a buck. There is such a thing as being too frugal. Insurance is one expense in particular that you should weigh the savings with the benefits

I’m sure there are plenty of other ways to trim expenses and increase your NOI, but those should get you going.

Laundromat Due Diligence

If you have made it this far you have basically just taken a due diligence masterclass. It’s not everything there is to know about due diligence, but it’s more than the vast majority of first-time owners (and multi-laundromat owners, for that matter) know when buying a laundromat. To learn more about laundromat analysis and valuation, as well as how to run your new laundromat and scale your laundromat empire, consider joining the Pro Membership to join the community of dedicated laundromat owners determined to find financial freedom through laundromat ownership. We’re all better when we work together!

{kind=link}